Did you know that foreclosure filings across the country rose by 26% in the first quarter of 2026 alone? If you’ve received a notice from your bank, you aren’t just another statistic. You’re likely feeling the heavy weight of legal jargon and the deep anxiety of what happens next for your family. It’s natural to feel overwhelmed when your credit score and your home are both on the line. However, selling house to stop foreclosure is often the most effective way to take back control before the auction clock runs out.

We understand that your primary goal is to protect your future and keep your financial reputation intact. This guide will show you how to navigate the complex landscape of current mortgage regulations, including the latest FHA loss mitigation rules and the new VA Partial Claim Program. We’ll explore how you can stop the foreclosure process, preserve your credit health, and potentially walk away with a clean slate. From understanding the 120-day rule to exploring as-is property acquisitions, you’ll find a clear, methodical path forward that prioritizes your peace of mind.

Key Takeaways

- Understand the specific stages of the legal timeline so you can identify exactly how much time you have before an auction occurs.

- Explore immediate relief options like reinstatement and forbearance that may provide the breathing room you need to make a calm decision.

- Compare the pros and cons of different exit strategies to see why selling house to stop foreclosure is often the fastest path to a clean slate.

- Learn about modern creative finance solutions, including “Subject-To” options, which can help you walk away even if you have little to no equity in your home.

- Discover the two critical numbers you must request from your lender today to accurately assess your property’s value and your total payoff amount.

Understanding Foreclosure: Why Selling Your House is a Strategic Solution

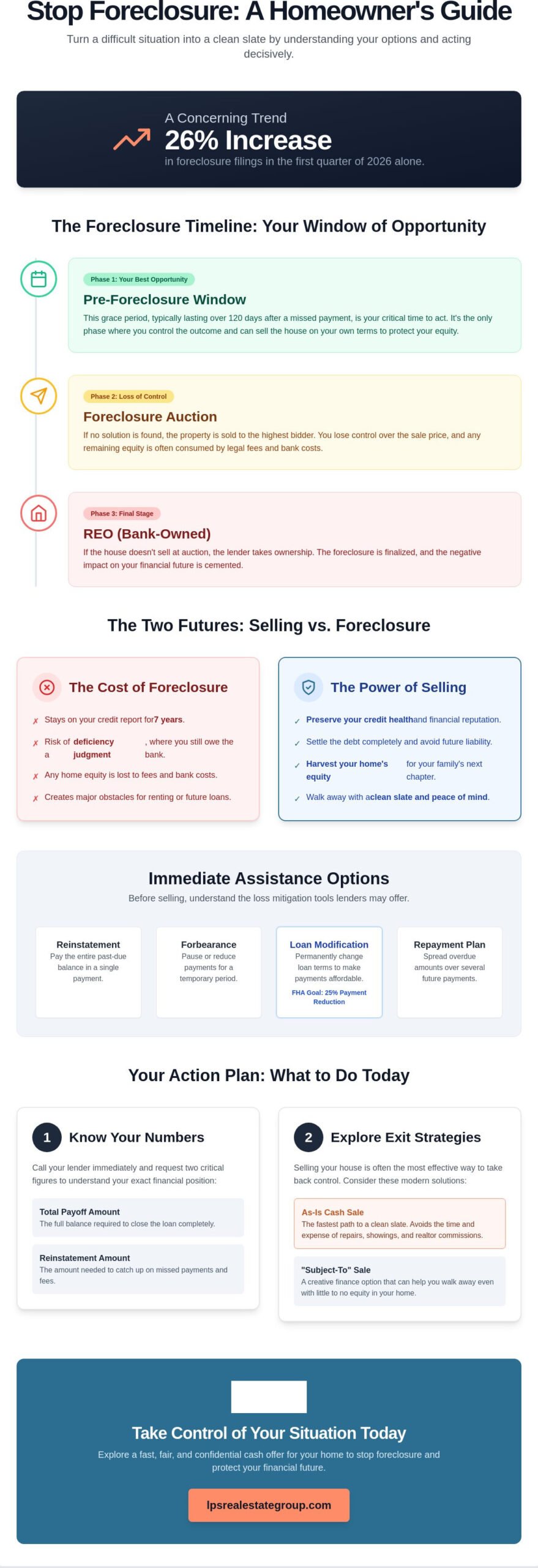

Foreclosure isn’t just a scary word; it’s a specific legal mechanism. Understanding the foreclosure process means recognizing that a lender is attempting to recover the balance of a loan because payments have stopped. While it feels like a personal loss, for the bank, it’s a recovery procedure. By choosing the path of selling house to stop foreclosure, you shift from being a passive participant in their process to being the decision-maker in your financial exit.

The journey usually moves through three distinct phases. First is pre-foreclosure, which begins the moment you miss a payment. If no solution is found, the property moves to the auction phase, where it’s sold to the highest bidder on the courthouse steps. If it doesn’t sell there, it becomes REO (Real Estate Owned) or bank-owned. The goal is to act before the auction occurs. This is the only way to ensure you have a say in the final sale price and the terms of your move.

Equity is your most powerful tool in this situation. It’s the difference between what your home is worth and what you owe the bank. Even a small amount of equity can be a lifesaver. It can provide the cash you need to pay for a security deposit on a new rental or cover moving expenses. If you wait until the auction, that equity often disappears into legal fees and bank costs. Selling early allows you to harvest that value for your family’s future.

The Pre-Foreclosure Window: Your Best Opportunity

This window is the time between your first missed payment and the official Notice of Sale. Federal law generally prohibits mortgage servicers from starting foreclosure proceedings until you’re more than 120 days delinquent. This gives you a four-month cushion to find a buyer. Lenders are often willing to work with sellers now because they want to avoid legal costs. Pre-foreclosure is the grace period for proactive homeowners to find a dignified way out.

How Foreclosure Impacts Your Financial Future

A completed foreclosure stays on your credit report for seven years. This makes it difficult to rent an apartment or buy a car. Beyond the credit score, there’s the risk of a deficiency judgment, where the bank sues you for the remaining balance. Choosing the option of selling house to stop foreclosure helps you avoid these scars. Using a strategy for selling a house in pre-foreclosure lets you settle the debt and walk away with a clean slate.

Behind on Mortgage Help: Exploring Your Immediate Assistance Options

Falling behind on payments feels like a weight that only gets heavier every month. Before you conclude that selling house to stop foreclosure is your only choice, it’s vital to understand the tools lenders use to keep people in their homes. These programs, often called loss mitigation, are designed to find a middle ground between the bank and the homeowner. By exploring these options early, you can decide whether you want to stay in the home or move toward a graceful exit.

- Reinstatement: This is the most direct solution. You pay the entire past-due balance, including interest and legal fees, in a single payment to bring the loan current.

- Forbearance: Your lender allows you to pause or reduce payments for a specific period. This is helpful for temporary hardships, but the missed payments are usually added back to the balance or required as a lump sum later.

- Loan Modification: The bank changes the original terms of your mortgage. This might involve lowering the interest rate or extending the loan length to make the monthly cost affordable. As of 2026, many FHA programs aim for a 25% reduction in monthly principal and interest payments for qualified borrowers.

- Repayment Plans: The overdue amount is spread out over several months and added to your regular mortgage payments until the account is caught up.

Government and Non-Profit Resources for Homeowners

You don’t have to face a massive financial institution by yourself. HUD-approved housing counselors act as free mediators to help you navigate these options. They can also guide you toward the Homeowner Assistance Fund (HAF), a federal program that provides financial aid to homeowners facing delinquency. Always consult official government guidance on avoiding foreclosure to verify which programs are active in your state. Be extremely cautious of “rescue” companies that demand upfront fees. Legitimate help from government-backed agencies is almost always free.

Communicating Effectively with Your Loan Servicer

It’s tempting to leave the certified mail from your bank unopened on the kitchen table. However, ignoring these notices only accelerates the legal process. When you’re ready to talk, approach the loss mitigation department with quiet confidence. Have a “hardship package” ready, which typically includes a hardship letter, your two most recent pay stubs, and your last two years of tax returns. Your hardship letter should be a brief, honest account of the circumstances that led to the missed payments. If the bank’s requirements feel like too much of a burden, you may want to look into a direct sale to resolve the debt on your own terms.

Comparing Exit Strategies: Traditional Sale vs. Cash Offer vs. Short Sale

When you’re facing a deadline, the strategy you choose for selling house to stop foreclosure determines how much control you keep. While a traditional sale is the standard for most homeowners, the foreclosure timeline moves much faster than the average real estate market. It’s important to weigh the benefits of a high sales price against the risk of the bank taking the property before you can even get to the closing table. Understanding the full foreclosure vs selling for cash comparison can help you make the most informed decision for your specific situation.

- Traditional Sale: This route offers the potential for the highest price. However, it requires the home to be in good condition, involves real estate agent commissions, and typically takes months to complete.

- Short Sale: If you owe more than the home is worth, the bank might allow a short sale. This requires their explicit approval; this is often a slow and emotionally draining process that doesn’t always stop an auction in time. If you want to avoid short sale delays and explore faster 2026 home exit options, there are alternatives worth considering.

- Direct Cash Offer: Speed and certainty are the main advantages here. There are no repairs needed, no commissions to pay, and you can often close in as little as a week.

- Deed in Lieu of Foreclosure: This is essentially handing the keys back to the lender. While it stops the auction, it’s a last resort that still leaves a significant mark on your credit report.

Why Speed Matters More Than ‘Top Dollar’ in Foreclosure

In a normal market, waiting an extra month for a better offer makes sense. In foreclosure, every day you wait adds interest and late fees to your total debt. If a traditional buyer’s mortgage takes 45 days to process, there’s a high risk the auction date will arrive before they’re ready. Choosing direct home buyers removes the “appraisal gap” risk; this is when a bank refuses to lend on a house because it doesn’t meet their strict value or condition standards.

The Reality of Selling a House ‘As-Is’

Selling “As-Is” means you don’t have to worry about cleaning, painting, or fixing structural issues. Distressed properties often struggle on the traditional MLS because most buyers are looking for move-in-ready homes. When a house needs work, traditional buyers often demand deep discounts or walk away after an inspection. Direct buyers calculate these repair costs into their offer from the start. This simplifies your life by removing the need for contractors or out-of-pocket expenses during an already stressful time. By selling house to stop foreclosure in its current condition, you save both time and the limited cash you have on hand.

Step-by-Step Guide to Selling Before the Auction Date

Managing a sale while a clock is ticking requires a methodical approach. You aren’t just selling a property; you’re executing a rescue mission for your credit and your future. The first and most critical step is to request a formal payoff statement from your lender. This document provides the exact amount needed to satisfy the debt, including any late fees, legal costs, and interest accrued since your last payment. Don’t rely on your monthly statement, as it won’t reflect the total cost of stopping the legal proceedings.

Once you have your payoff number, you must determine the home’s value in its current state. If you decide that selling house to stop foreclosure is your best path, you’ll need to choose a sales method based on your timeline. If the auction is months away, a traditional listing might work. If you’re only weeks from the auction date, a direct sale is often the only way to ensure the deal closes in time. After you sign a purchase agreement, immediately notify your lender’s legal department. They need proof of the pending sale to consider pausing the foreclosure process. Finally, you’ll close the sale through a title company or attorney, ensuring the lender is paid directly and the lien is released.

Requesting a Foreclosure Postponement

A valid, signed sales contract is a powerful negotiation tool. In many cases, banks are willing to grant a 30-day stay of the auction if you can prove that a closing is imminent. Banks prefer a paid-off loan over a foreclosed property. Your closing attorney or title company will usually handle this communication, providing the bank with the necessary paperwork to show the sale is legitimate and funded. If you need a fast, reliable contract to show your lender, you can get a cash offer today to start this process immediately.

Calculating Your Net Proceeds

It’s important to have a realistic view of the numbers. To find your net proceeds, subtract the payoff amount, any back taxes, and any other liens from the final offer price. While everyone hopes to walk away with a large check, sometimes “breaking even” is a massive victory. It means you’ve successfully avoided a seven-year credit scar and a deficiency judgment. If the sale price exceeds your debt, the remaining cash is yours to keep, providing you with a foundation for your next chapter. This clean slate is the ultimate goal of selling house to stop foreclosure.

Creative Finance: A Modern Path to Foreclosure Relief

Traditional sales often require significant equity to cover real estate commissions, closing costs, and repair bills. If you owe nearly what your home is worth, or even slightly more, you might feel like you have no options left. This is where creative finance, specifically a “Subject-To” arrangement, becomes a powerful tool. In this scenario, the buyer takes over your existing mortgage payments. While the loan stays in your name for a period, the buyer becomes legally responsible for making the payments, providing you with immediate relief from the monthly financial burden.

LPS Real Estate Group specializes in these complex, time-sensitive scenarios. We recognize that selling house to stop foreclosure isn’t always a simple math equation. Our Creative Finance Solutions allow us to step in and help homeowners who are “underwater” or have very little equity. By taking over the payments, we stop the foreclosure clock instantly. This protects your credit from the devastating impact of a completed auction and ensures the lender receives what they’re owed without further legal action.

Is Creative Finance Safe for Sellers?

Safety and transparency are the foundations of a successful creative deal. We always prioritize using professional title companies and provide full legal disclosures so you understand every step of the process. You might have heard of the “Due on Sale” clause, which technically allows a bank to request full payment if a property’s title changes. Professional investors manage this by maintaining a perfect payment history, which keeps the lender satisfied. We view this as a partnership. Our goal is to create a win-win situation where your debt is handled with integrity and your financial future is preserved.

Moving Forward: Life After the Sale

The true benefit of selling house to stop foreclosure through creative means is the peace that follows. Once the agreement is signed and the payments are handled, the constant stream of collection calls and certified letters finally stops. You can breathe again. This is your opportunity to start planning your next move with a clean financial slate and a sense of control. It’s vital to remember that you are not your mortgage; a difficult financial season doesn’t define your worth. By taking action now, you’ve chosen a path of resilience. You’ve protected your credit health and cleared the way for a fresh start, proving that there is always a way forward when you have the right guide.

Take the First Step Toward a Fresh Start

You’ve seen that the foreclosure process is a timeline with specific windows of opportunity rather than an immediate trap. Whether you pursue a loan modification or decide that selling house to stop foreclosure is the most reliable way to protect your credit score, the most important step is to act while you still have choices. By understanding your payoff amount and exploring modern exit strategies like creative finance, you can move from a state of anxiety to one of clear, manageable progress.

At LPS Real Estate Group, we serve as professional foreclosure prevention specialists with a national reach and local closing expertise. We’re here to provide compassionate, jargon-free consultations that respect your unique circumstances and prioritize your peace of mind. You don’t have to navigate these bank notices alone. Request a transparent, no-obligation cash offer from LPS Real Estate Group today to see how we can help you settle your debt and walk away with a clean slate. Your future is worth more than a mortgage balance, and a brighter financial chapter is well within your reach.

Frequently Asked Questions

Can I sell my house if I’ve already received a Notice of Default?

Yes, you can absolutely sell your home after receiving a Notice of Default. You remain the legal owner of the property until the foreclosure auction is officially completed and the deed is transferred. Acting quickly during this stage allows you to settle your debt on your own terms rather than letting the bank dictate the outcome. It’s often the best way to regain a sense of control over your financial situation.

How long do I have to sell my house before the bank takes it?

You generally have at least 120 days from your first missed payment before a servicer can legally start the foreclosure process. This federal protection is designed to give you time to explore loss mitigation options. Once a Notice of Sale is issued, the remaining time depends on your specific state laws, but it’s often a matter of weeks. Securing a signed purchase agreement is the most reliable way to request a postponement from your lender.

What is the difference between pre-foreclosure and foreclosure?

Pre-foreclosure is the “warning” phase where you still have the opportunity to catch up on payments or sell the property yourself. Foreclosure is the final legal action where the lender takes possession of the home through a public auction. Distinguishing between these stages is vital because pre-foreclosure offers the most flexibility for a graceful exit. Selling house to stop foreclosure is much easier to navigate during the pre-foreclosure window before legal fees begin to pile up.

Can I sell my house for less than I owe on the mortgage?

Yes, you can sell for less than the mortgage balance through a short sale or creative finance strategies. A short sale requires your lender’s approval to accept a lower amount as full payment of the debt. Alternatively, you can explore “Subject-To” arrangements where a buyer takes over your existing payments. These options are particularly helpful for homeowners who have little to no equity but still want to avoid a total credit loss.

Will selling my house stop the foreclosure auction immediately?

A completed sale stops the auction, but merely listing the home on the market does not pause the legal clock. You must provide your lender’s legal department with a signed, valid purchase contract to request a formal stay of the sale. Banks are usually willing to wait if they see a clear path to being paid in full through a pending closing. This is why speed and certainty are so important when you’re selling house to stop foreclosure.

Do I need to make repairs before selling to a cash buyer?

No repairs are necessary when you choose to work with a professional cash buyer. These entities specialize in as-is property acquisitions, meaning they factor the cost of cleaning, painting, and structural fixes into their initial offer. This approach removes the burden of finding renovation funds when you’re already facing financial pressure. You can walk away from the property exactly as it sits today without spending a dime on contractors.

What happens to my credit score if I sell my house to stop foreclosure?

Selling your home helps you avoid the most severe credit damage, which is the official “Foreclosure” mark that stays on your report for seven years. While your score will still reflect the missed payments that led to this situation, a settled debt is viewed much more favorably by future lenders. Avoiding a foreclosure auction means you can often qualify for a new mortgage much sooner than if you had let the bank take the property.

Are there any programs that help with mortgage payments in 2026?

Several specialized programs are active in 2026, including the VA Partial Claim Program which provides interest-free loans to help veterans bring their mortgages current. FHA borrowers can also benefit from a revised “waterfall” loss mitigation process that aims to reduce monthly payments by 25%. These initiatives are designed to provide a safety net, but it’s important to apply early before the 120-day delinquency window expires and legal action begins.

One Response