What if the default notice in your mailbox isn’t the end of your homeownership story, but actually a 120-day window to take back control? With foreclosure filings up 26% in early 2026, many homeowners are currently asking how to sell a house in pre-foreclosure before the bank takes over. It’s completely normal to feel overwhelmed by lender phone calls and confusing legal terms. You’re likely focused on protecting your credit and finding a way to move forward without losing everything you’ve built. We understand that the fear of the unknown is often heavier than the financial burden itself.

This guide is designed to help you navigate this transition with clarity and confidence. We believe that a difficult financial season shouldn’t define your future. You’ll discover how to stop the foreclosure clock, potentially walk away with your equity intact, and keep your credit score ready for your next home. We will break down the 2026 selling process into simple, manageable steps so you can make the best decision for your family’s peace of mind.

Key Takeaways

- View the “Notice of Default” as a formal starting gun that gives you a specific window to act and regain control of your financial future.

- Understand the critical differences between a traditional sale and a direct cash offer, focusing on speed and the ability to sell your home in its current condition.

- Discover the specific steps for how to sell a house in pre-foreclosure, starting with finding your true payoff amount to understand your equity position.

- Explore creative finance solutions like “Subject-To” purchases that can stop a foreclosure immediately, even if you have little to no equity in the property.

- Learn how to protect your credit score and housing future by choosing a dignified exit strategy that stops the bank auction process.

What Is Pre-Foreclosure and Why Is It Your Window of Opportunity?

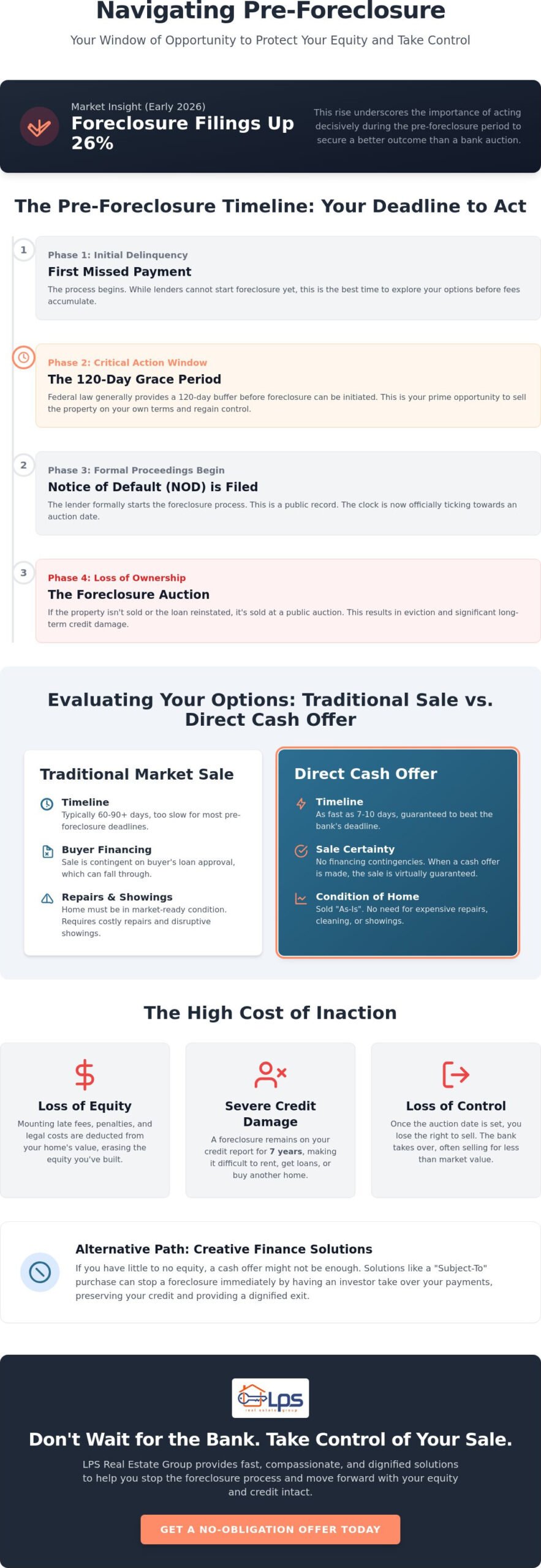

Pre-foreclosure is the period between your first missed mortgage payment and the final auction date. It’s a high-stakes time, but it’s also your most important window of opportunity. During this phase, you still legally own your home. You have the right to live there, and you have the absolute right to sell it on your own terms. The formal process typically begins with a Notice of Default (NOD). This document is essentially a formal warning from your lender. It’s the starting gun that signals you need to act. For many, the focus becomes learning how to sell a house in pre-foreclosure to protect their credit and move forward with dignity.

Pre-Foreclosure vs. Foreclosure: Knowing the Difference

It’s helpful to distinguish between a status and an action. Pre-foreclosure is a status that describes where you are in the timeline. Foreclosure is the actual legal action that ends your ownership. While you’re in the pre-foreclosure stage, you still hold the steering wheel. You have more negotiation power now than you will at any other point in the process. Lenders generally prefer a private sale over the long, expensive understanding the foreclosure process because they’d rather have the cash than a property they have to maintain and sell themselves. By finding a buyer now, you’re actually helping the bank solve a problem while saving your own equity.

The Impact of Doing Nothing: Why Time Is Your Most Valuable Asset

Ignoring the problem doesn’t make it go away; it makes it more expensive. Late fees, interest, and legal costs compound quickly. These costs directly reduce the amount of equity you’ll walk away with after a sale. You may also see a “Lis Pendens” filed against your property in public records. This is a public notice that tells the world a legal claim exists against your home. It’s a stressful mark to have, but it isn’t permanent yet.

If you allow the bank to complete the auction, that foreclosure will stay on your credit report for seven years. This makes it much harder to rent a new apartment or buy another home later. Taking action during the 120-day pre-foreclosure window is the best way to stop the clock. It preserves your future housing options and ensures you aren’t forced out on someone else’s timeline. Understanding how to sell a house in pre-foreclosure isn’t just about a transaction; it’s about reclaiming your financial independence. For a deeper look at how selling a house to stop foreclosure can protect your credit and preserve your equity, our comprehensive 2026 resource guide walks you through the latest mortgage regulations and loss mitigation options.

The Pre-Foreclosure Timeline: Understanding Your Deadline to Act

Time is your most significant asset when facing financial challenges with your mortgage. While it may feel like the bank is rushing you, federal law actually provides a specific safety buffer. Lenders generally must wait until you are more than 120 days delinquent on your mortgage before they can officially initiate foreclosure proceedings. This 120-day window is a critical period. It’s your best opportunity to learn how to sell a house in pre-foreclosure without the added pressure of an imminent auction date. Understanding this timeline allows you to move from a place of reaction to a place of strategic planning.

During this period, you’ll encounter the “reinstatement period.” This is a timeframe where you can stop the entire process by paying the total amount you’re behind, including late fees and interest. If you can’t reinstate the loan, you still have the right to sell the property. There are several government-backed options to avoid foreclosure that can provide temporary relief while you arrange a sale. If you’re feeling pressured by these deadlines, exploring foreclosure prevention options can help you find a path forward before the clock runs out.

Judicial vs. Non-Judicial Foreclosure Processes

The speed of your timeline depends heavily on whether your state uses a judicial or non-judicial process. In a judicial foreclosure, the lender must file a lawsuit to take the home. This process is common in states like Florida or New York and often takes much longer, sometimes lasting over a year. A non-judicial foreclosure happens outside of the court system using a “power of sale” clause in your mortgage contract. This is common in states like Texas or Georgia. It moves significantly faster, sometimes concluding in just a few months. It’s vital to check your specific state laws, as the national average timeline to complete a foreclosure was 592 days at the end of 2025, but local rules vary wildly.

Key Milestones That Trigger Legal Action

Lenders follow a methodical sequence of markers before they take your home. Understanding these milestones helps you gauge how much time you truly have left to find a buyer.

- 30-60-90 Day Delinquency: These are the standard markers where lenders send increasingly urgent demand letters and assess late fees.

- Notice of Intent to Foreclose: This is a formal warning letter sent before the legal process starts, giving you one last chance to catch up.

- Notice of Default (NOD): This is the official document filed with the county recorder that marks the beginning of the public pre-foreclosure phase.

The Notice of Trustee Sale serves as your final warning, establishing the exact date and time the property will be sold at a public auction. Once this notice is posted, your window for how to sell a house in pre-foreclosure narrows significantly. Acting before this notice appears ensures you have the leverage to negotiate a fair price and protect your equity.

Evaluating Your Options: Traditional Sale vs. Direct Cash Offer

Deciding how to move forward is often the most stressful part of the pre-foreclosure journey. You’re balancing the need to maximize your home’s value with the reality of a ticking clock. When considering how to sell a house in pre-foreclosure, you generally have two paths: listing the property on the open market or accepting a direct cash offer. Each path serves a different set of priorities. A traditional sale aims for the highest price, while a direct buyout prioritizes speed and certainty to stop the bank’s progress immediately.

When a Traditional Listing Makes Sense

A traditional market listing is usually only viable if you have significant equity and at least three to four months of lead time. Most traditional buyers require 45 to 60 days to close due to mortgage underwriting and inspections. You must also be able to keep your mortgage payments current during the listing period to prevent the bank from advancing the foreclosure date. For a deeper dive on the mechanics of a quick sale, you can read our Sell My House Fast for Cash: The Definitive 2026 Homeowner’s Guide. If your timeline is shorter than 90 days, a traditional listing might be too risky.

The Advantages of a Direct Cash Sale in Pre-Foreclosure

A direct cash offer is often the most reliable way to stop an auction. These deals can close in as little as 7 to 14 days, providing a swift resolution that a financed buyer simply cannot match. This option eliminates several hurdles that often sink traditional deals for homes in distress:

- As-Is Acquisition: Traditional buyers often want “move-in ready” homes. Cash buyers purchase the property in its current condition, so you don’t have to spend money on repairs you can’t afford.

- Reduced Costs: You avoid the standard 5.4% to 5.5% real estate commission and the typical 1% to 3% in seller closing costs.

- Privacy and Convenience: You skip the stress of public showings and open houses. You can often stay in the home until the day of closing without the disruption of strangers walking through your living room.

In cases where you owe more than the property is worth, you may need to pursue a short sale. It’s helpful to understand the legal definition of a pre-foreclosure sale, which involves the lender agreeing to accept less than the full payoff amount. Whether you have equity or are facing an “equity gap,” choosing a direct buyout offers a no-contingency path that provides peace of mind when the bank is threatening action. If you want to explore faster alternatives before committing to a lengthy bank-approval process, our guide on how to avoid a short sale and compare your 2026 home exit options breaks down every available path side by side. Knowing how to sell a house in pre-foreclosure through a direct purchase gives you a dignified exit strategy on your own terms.

How to Sell a House in Pre-Foreclosure: A 5-Step Action Plan

Taking the first step is often the hardest part of the journey. When you’re learning how to sell a house in pre-foreclosure, having a clear roadmap can turn a chaotic situation into a manageable process. This five-step plan is designed to help you move from feeling stuck to feeling empowered. By following these logical stages, you can navigate the complexities of the 2026 housing market with confidence.

- Step 1: Determine your “Payoff Amount.” Don’t just look at your last monthly statement. Request a formal payoff letter from your lender that includes the principal balance, accumulated interest, late fees, and any legal costs associated with the default.

- Step 2: Get an as-is valuation. You need to know what your home is worth in its current state. Understanding your equity position helps you decide if a traditional sale will cover your debts or if you need to explore other avenues.

- Step 3: Communicate with your lender. Reach out to request a “Foreclosure Postponement.” If you can prove you have a viable sales plan or a signed contract, many lenders will pause the legal process to allow the sale to close.

- Step 4: Choose your sales path. Decide between a direct cash buyer for speed, a short sale if you’re underwater, or a traditional listing if you have the time and equity.

- Step 5: Close the sale. Finalize the transaction and ensure your lender provides a “Satisfaction of Mortgage.” This document is your proof that the debt is fully settled and the lien is released.

How to Talk to Your Lender Without Panic

Lenders view a house in default as a non-performing asset. They generally don’t want to own your property; they want the loan settled. When you call, ask specifically for the Loss Mitigation Department. These professionals are trained to help homeowners find alternatives to auction. Prepare a Hardship Letter before you call. This document should clearly and honestly explain the circumstances that led to the missed payments, such as a medical emergency or job loss. Demonstrating a proactive plan for how to sell a house in pre-foreclosure often makes them more willing to work with you.

Calculating Your Net Proceeds

To calculate your net proceeds, subtract the total payoff amount and all selling costs from the final offer price. Keep in mind that selling costs typically range from 9-10% of the sale price in a traditional transaction, with seller closing costs accounting for 1-3%. If the house is worth less than the debt, you’re facing a short sale, which requires lender approval. Before committing to that path, it’s worth reviewing your options to avoid a short sale entirely by comparing faster 2026 exit strategies that don’t require bank approval of the final price. If your current situation is the result of a family transition, you might find our guide on how to sell an inherited property helpful for navigating those specific legal hurdles. For families managing an estate where the property is already in the court system, understanding the cost to sell a house in probate can help you anticipate additional fees and timelines that may affect your net proceeds. If you need a faster resolution to stop the clock immediately, you can request a fair cash offer to see where you stand.

Creative Finance Solutions: When a Cash Offer Isn’t Enough

Not every homeowner has enough equity for a traditional sale or a standard cash offer to make sense. If you bought your home recently or the market has shifted, you might find that you owe nearly as much as the home is worth. This is where creative finance provides a path forward. It’s a specialized way for how to sell a house in pre-foreclosure when traditional methods fail. These solutions focus on the debt itself rather than just the property value. They allow you to move on without having to bring money to the closing table. If you want to understand all of your available options under the latest 2026 mortgage regulations, our guide on selling your house to stop foreclosure covers FHA loss mitigation rules and the new VA Partial Claim Program in detail.

What Is a “Subject-To” Sale?

In a “Subject-To” transaction, a buyer takes over your existing mortgage payments while the title transfers into their name. The loan stays in your name for a period, but the investor becomes responsible for the monthly principal, interest, taxes, and insurance. This stops the foreclosure clock instantly. Because the investor brings the arrears current, it immediately halts the bank’s legal proceedings.

There is a significant benefit to your credit score with this approach. As the investor makes consistent, on-time payments, your credit history begins to reflect a positive payment trend. This is a powerful alternative for those who need to move but cannot afford the high costs of a traditional sale. It’s a win-win strategy that solves the bank’s problem while giving you a fresh start. If the property is part of a larger estate, it’s also worth reviewing the real cost to sell a house in probate in 2026, as court filing fees and statutory legal costs can significantly reduce what heirs ultimately receive.

The LPS Real Estate Group Approach to Foreclosure Prevention

We specialize in these complex, non-traditional exits because we understand that every financial situation is unique. Our team prioritizes a “Transparency First” promise. We ensure you understand exactly how the process works through empathy-driven consultations. We handle as-is properties regardless of their condition, code violations, or the amount of work needed. You don’t have to worry about cleaning, repairs, or dealing with difficult lenders alone.

Finding the right partner is essential when navigating how to sell a house in pre-foreclosure using creative finance. It requires a buyer with the experience to handle bank negotiations and title complexities with integrity. We act as your trusted advisor, listening to your needs first and providing a clear path to your next chapter. If you’re ready to explore a dignified exit that protects your future housing options, we’re here to help. Get a fair, no-obligation offer from LPS Real Estate Group today to see which solution fits your needs best.

Reclaiming Your Financial Future and Peace of Mind

Navigating the 120-day pre-foreclosure window requires a shift from fear to strategic action. You’ve learned that the Notice of Default is simply a signal to evaluate your options; it’s a window where you still hold the power to choose your path. Understanding how to sell a house in pre-foreclosure allows you to protect your equity and, more importantly, your housing future. Whether you opt for a traditional sale or a specialized creative finance solution, taking the first step is what prevents a permanent mark on your credit report.

At LPS Real Estate Group, we carry an A+ rating for our commitment to transparency and empathy. We’re specialists in creative finance and Subject-To offers, providing solutions that traditional agents often can’t. Our team can often close in as little as 7 days, ensuring you beat the auction clock and move forward on your own terms. You don’t have to face this transition alone. We’re here to listen and help you find the most dignified path forward for your family. Request your fair cash offer and stop foreclosure today. Remember that this difficult season is just a chapter, not the final page of your story.

Frequently Asked Questions

Can I sell my house if I have already received a Notice of Default?

Yes, you can absolutely sell your home after receiving a Notice of Default. Receiving this document means the formal legal process has begun, but you remain the legal owner with the full right to transfer the title. It’s often the most strategic time to act because you still have the leverage to negotiate a sale on your own terms before an auction date is set.

How long do I have to sell my house once pre-foreclosure starts?

The timeline varies by state, but you generally have a critical 120-day window from your first missed payment before the bank can officially initiate foreclosure. Once the Notice of Default is filed, the clock moves faster, often leaving you with 90 days or less. The national average time to complete a foreclosure was 592 days in late 2025, but local rules for non-judicial states can be much shorter.

Will selling my house in pre-foreclosure ruin my credit?

Selling your home is significantly better for your credit than allowing a completed foreclosure to occur. While missed payments will impact your score, a successful sale shows that the debt was settled or paid in full. This allows you to avoid the seven-year mark that a formal foreclosure leaves on your record, making it easier to secure housing in the future.

What is a short sale, and should I consider one?

A short sale occurs when the lender agrees to accept a sale price that’s lower than your remaining mortgage balance. You should consider this path if your home’s value has dropped below what you owe. It’s a complex process that requires lender approval, but it serves as a vital tool for those wondering how to sell a house in pre-foreclosure when they have little to no equity.

Do I need to make repairs before selling to a cash buyer?

You don’t need to make any repairs when selling to a professional cash buyer. We specialize in as-is property acquisition, meaning we take on the burden of cleaning, fixing code violations, or handling structural issues. This saves you the out-of-pocket costs and the months of time you likely don’t have when an auction clock is ticking.

Can the bank stop me from selling my house in pre-foreclosure?

The bank generally cannot stop you from selling as long as the sale price covers the total payoff amount, including interest and fees. Lenders actually prefer a private sale because it’s faster and less expensive for them than a public auction. If you’re pursuing a short sale, they must approve the final offer, but they’re often motivated to agree to avoid a non-performing asset.

What happens to my equity if I sell during pre-foreclosure?

Any equity remaining after the mortgage payoff, late fees, and selling costs belongs entirely to you. Selling early in the pre-foreclosure phase is the most effective way to protect this money. The longer you wait, the more your proceeds are reduced by compounding interest, daily penalties, and the bank’s mounting legal fees.

How quickly can LPS Real Estate Group close on a pre-foreclosure property?

We can often close on a property in as little as 7 days. This speed is essential for homeowners who have an auction date looming and need a guaranteed exit. Our team focuses on a clear, methodical process to ensure the how to sell a house in pre-foreclosure journey ends with you walking away with a fresh start before the bank takes further action.

7 Responses