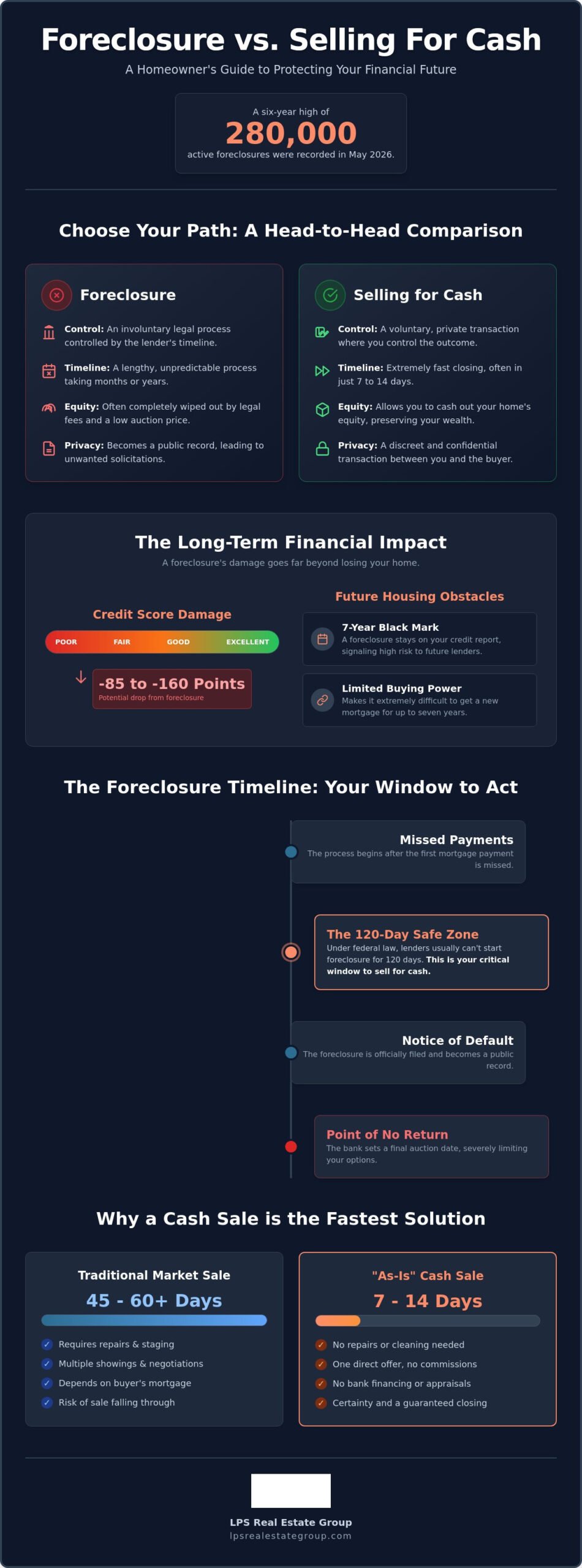

With 280,000 active foreclosures reaching a six-year high in May 2026, you aren’t alone if you’re feeling the weight of a mortgage that’s become unmanageable. It’s easy to feel trapped when the foreclosure vs selling for cash debate feels like a choice between two difficult unknowns. You might be worried about where you’ll live next or how a legal mark on your record will follow you for the next seven years. We understand that this stress often comes from factors outside your control, like the recent surge in property insurance and taxes that now account for nearly half of many monthly housing payments.

We’re here to help you navigate this transition with clarity and confidence. This guide will explain the long-term impacts of both paths so you can protect your financial future and your peace of mind. We’ll explore how the 120-day delinquency window works under federal law and compare the potential 160-point credit drop of a foreclosure against the recovery potential of a cash sale. You’ll learn how taking an active step today can help you save your equity, protect your credit for future housing, and secure a certain path forward.

Key Takeaways

- Understand the fundamental differences in the foreclosure vs selling for cash debate to see which path protects your equity and future housing options.

- Learn how a foreclosure can impact your credit score by up to 160 points and limit your ability to buy a new home for seven years.

- Discover how a cash sale can be completed in as little as 7 to 14 days, providing a fast exit that stops the legal process.

- Compare the financial reality of both options, including how to avoid commissions and repairs through a direct as-is property acquisition.

- Identify the “Safe Zone” in the foreclosure timeline so you can take action before the bank sets a final auction date.

Foreclosure vs. Selling for Cash: Understanding Your Options

When you’re facing the possibility of losing your home, the situation often feels like a choice between two entirely different worlds. Foreclosure is a legal process where your lender repossesses the property because payments hasn’t been made. It’s an involuntary action that moves according to the bank’s schedule. On the other hand, a cash sale is a private, voluntary transaction with an investor who has the funds ready to go. When weighing foreclosure vs selling for cash, the primary difference lies in who holds the power over the timeline and the final outcome.

Many homeowners describe a “frozen” sensation when that first notice of default arrives. The legal jargon and formal letters can feel overwhelming, often leading people to wait and hope for a miracle. However, this is the most critical time to consider equity preservation. If you’ve paid down your mortgage or your home’s value has increased, that equity belongs to you. Selling the property before the bank takes it allows you to walk away with some of that value, whereas a foreclosure auction often wipes it out entirely. Selling now isn’t giving up; it’s a strategic move to secure your next chapter.

The Legal Mechanics of Foreclosure

The path to a public auction follows a strict legal sequence that starts long before the sheriff arrives. Under federal law, specifically the CFPB’s Regulation X, a mortgage servicer usually can’t start the process until you’re more than 120 days delinquent. This gives you a four-month window to find a solution. Depending on your state, you might face a judicial process, which goes through the court system, or a non-judicial process, which is often faster. A deeper look into understanding the foreclosure process shows that once the auction date is set, your options narrow significantly. That date represents the absolute point of no return for your ownership.

The Cash Sale Alternative

Choosing a cash sale offers a way to bypass the hurdles of a traditional real estate transaction. In a typical market sale, a buyer needs 45 to 60 days to secure mortgage approval, which is time you simply don’t have when an auction is looming. Cash buyers use their own capital, allowing for a closing in as little as 7 to 14 days. This speed is why many people find it to be the most viable path when comparing foreclosure vs selling for cash.

One of the biggest reliefs for homeowners is the “as-is” nature of these purchases. You don’t need to worry about fixing a leaking roof or updating an old kitchen to find a buyer. This is vital because the clock is always ticking during the pre-foreclosure phase. Since speed is the most critical factor when selling a house in foreclosure, removing the need for repairs and bank inspections can be the difference between saving your credit and losing everything.

The True Cost of Foreclosure: Why It Is More Than Just Losing a Home

Losing a home is a deeply personal experience, but the impact of a foreclosure extends far beyond the front door. It’s a legal event that creates a ripple effect throughout your entire financial life. When you compare foreclosure vs selling for cash, you have to look at the years of recovery that follow a bank-led repossession. While the immediate loss is the property itself, the secondary costs often include a loss of privacy and a significant blow to your future purchasing power.

The most immediate damage appears on your credit report. Data from 2026 shows that a foreclosure can lower your credit score by 85 to 160 points. If you started with a higher score, you’ll likely see the steepest drop. This mark remains on your report for seven years, acting as a “black mark” that tells future lenders you’re a high-risk borrower. In contrast, a short sale or a cash sale typically results in a smaller hit, usually between 50 and 150 points. Choosing to act early isn’t just about the house; it’s about protecting your ability to move forward.

The emotional toll is equally heavy. Once a notice of default is filed, it becomes a matter of public record. This often leads to a flood of unwanted solicitations and the stress of knowing your private financial struggle is visible to neighbors and the community. If you feel overwhelmed by these notices, exploring government programs to avoid foreclosure can provide a starting point for understanding your rights before the situation escalates further.

Long-Term Financial Consequences

A foreclosure doesn’t just make it hard to buy a new house; it makes it hard to live your life. Most conventional lenders require a seven-year waiting period before you can qualify for a new mortgage. Even if you look toward FHA or VA loans, you’re still looking at a two to three-year wait. Beyond housing, many employers now conduct credit checks as part of their background screening. A foreclosure can signal financial instability to a potential employer, potentially limiting your career growth. You may also face higher premiums for car insurance and much higher interest rates on any future credit cards or personal loans.

Deficiency Judgments and Tax Implications

If your home sells at auction for less than what you owe, the lender may be able to sue you personally to collect the remaining balance through a deficiency judgment. This means the bank can pursue your other personal assets or even garnish your wages to make up the difference. There is also a “Cancellation of Debt” tax trap to consider. The IRS often views the amount of debt the bank forgives as taxable income. This could leave you with a surprise tax bill at the end of the year. Selling for cash allows you to settle the debt on your own terms and often avoids these aggressive collection tactics. If you’re feeling pressured by the clock, you can reach out to us for a quiet, confidential conversation about your options.

Selling a House in Foreclosure for Cash: A Strategic Comparison

When you’re standing at a crossroads, the choice between foreclosure vs selling for cash isn’t just a financial decision; it’s a strategic one. Foreclosure is a slow, grinding process that can last for months, leaving you in a state of constant anxiety. A cash sale moves at your pace, often closing in as little as 7 to 14 days. This speed is essential because it stops the clock on the bank’s legal proceedings before they reach the point of no return. By choosing a faster path, you’re not just selling a property; you’re buying back your peace of mind.

Financial clarity is another major advantage of a direct sale. In a foreclosure, you might be hit with legal and filing fees ranging from $2,000 to $5,000, which are simply added to your default balance. A cash sale involves a direct purchase with $0 in commissions and no hidden closing costs. You also regain control over your life. Instead of being evicted on the bank’s schedule, you choose the move-out date that works for your family. Plus, because the sale is “as-is,” you don’t have to spend a dime on repairs or cleaning. You can take what you want and leave the rest to the buyer.

Cash Offer vs. Traditional Listing

Many homeowners consider listing their home on the MLS, but this is often a risky move when you’re in pre-foreclosure. Traditional sales are slow. They require open houses, inspections, and buyers who need to secure their own financing. In July 2026, with mortgage rates for 30-year fixed loans averaging around 6.49%, many retail buyers struggle to get approved. If their financing falls through at the last minute, you could lose the narrow window of time you had to save your credit. By working with a direct buyer, you can avoid a short sale and the uncertainty of the open market entirely.

Cash Sale vs. Foreclosure Outcomes

The final outcome is where the two paths diverge most sharply. A foreclosure often results in “equity stripping.” This term describes when the bank’s accumulated fees, late penalties, and the low auction price eat away all the value you’ve built in the home, leaving you with nothing. A cash sale focuses on equity preservation, allowing you to walk away with cash in hand to start your next chapter. It also keeps your business private. While an auction is a public event, a cash sale is a confidential transaction. This keeps your financial situation off the public record and away from unwanted attention.

Timing Your Exit: When to Stop Fighting and Start Selling

Deciding when to stop fighting for a home you can no longer afford is one of the most difficult emotional hurdles you’ll face. Many homeowners spend months in a state of “survival mode,” trying every possible avenue to keep their property. However, there is a point where fighting becomes counterproductive. In the foreclosure vs selling for cash debate, timing is your most valuable asset. The goal is to identify the “Safe Zone,” which is the window of time after receiving a notice of default but before an official auction date is scheduled. Acting within this window allows you to maintain control over the transition rather than letting the bank dictate your move-out day.

The “Wait and See” approach is particularly dangerous in 2026. With foreclosure filings increasing by 26% in the first quarter of this year, lenders are dealing with a higher volume of cases and may move more aggressively once the initial legal requirements are met. You should also be wary of loan modification offers that feel like stalling tactics. If a lender offers a modification that only lowers your payment by a small amount while adding years of interest to your balance, it may not be a true solution. If you’re unsure where you stand, it’s helpful to get a fair cash offer today to see if a direct sale provides a cleaner path forward.

Evaluating Your Equity

Your first step is to determine how much value is actually left in your home. Start by getting a clear payoff quote from your lender, which includes the principal, late fees, and any legal costs they’ve already incurred. Subtract this total from the current market value of your home. If the number is positive, you have equity to protect. If you owe more than the house is worth, don’t lose hope. We often utilize creative finance solutions to help homeowners in these specific situations. The key is to start the process of selling house to stop foreclosure before the legal window closes and your equity is consumed by mounting bank fees.

Communication with the Lender

Lenders are businesses, and they generally don’t want to own your house. Foreclosure is an expensive and time-consuming process for them. If you decide to pursue a cash sale, providing your lender with a “Notice of Intent to Sell” along with a signed purchase agreement can often pause the legal clock. This document shows the bank that a concrete solution is in progress. Lenders typically prefer a certain, fast closing over the uncertainty of a public auction. However, if you receive a “Notice of Trustee Sale,” you must act immediately. At this stage, the bank has set a final date, and every day you wait reduces your ability to negotiate a private exit.

How LPS Real Estate Group Facilitates a Stress-Free Cash Sale

At LPS Real Estate Group, we recognize that you’re facing a difficult season, not just a financial transaction. Our empathy-first approach means we start by listening to your specific story without judgment. We know that the choice between foreclosure vs selling for cash is often forced by circumstances like rising taxes or unexpected life changes. Our goal is to provide a sense of relief by offering a transparent, straightforward path out of a stressful situation. We act as a compassionate partner, ensuring you feel heard and respected throughout the entire process.

Transparency is the foundation of every offer we make. When you work with us, you won’t encounter hidden fees, commissions, or the pressure to perform repairs. By choosing an as-is property acquisition, you bypass the need for expensive cleaning or staging that traditional buyers usually demand. We provide a 7-day closing promise, which is designed to stop the foreclosure process in its tracks before the bank can take further legal action. This speed provides the certainty you need to protect your housing future and move forward with clarity.

Tailored Exit Strategies

Every property has a unique history, and we’re equipped to handle complex situations that might scare away traditional buyers. We have extensive experience with properties in probate or those facing complicated title issues. If you have little or no equity in your home, our creative finance solutions can provide a way out. We often utilize “Subject-To” agreements, where we take over your existing mortgage payments. This method allows us to settle the delinquency and keep your credit from suffering the long-term damage of a completed foreclosure.

Get Started Today

We’ve simplified our process into three manageable steps to keep your stress levels low. First, you contact us for an initial conversation about your situation. Second, we conduct a brief, respectful inspection of the property. Third, we present you with a fair cash offer and a clear timeline for closing. Taking this first step today is about more than just a house sale; it’s about preserving your options for tomorrow. The sooner we begin, the more leverage we have to work with your lender and secure a positive outcome. Get your fair cash offer from LPS Real Estate Group today and start your journey toward financial recovery.

Take Control of Your Housing Future

Choosing your path when facing mortgage delinquency is about more than just the house; it’s about protecting your long-term stability. While foreclosure can feel like an inevitable ending, it’s actually a process that you can interrupt. By acting before the legal window closes, you can avoid the seven-year credit damage and the public nature of an auction. Selling for cash allows you to preserve your remaining equity and move out on your own terms, providing a fresh start that a bank repossession simply cannot offer.

At LPS Real Estate Group, we’ve spent over 8 years helping homeowners navigate these complex situations. We specialize in as-is property acquisitions and offer a transparent, commission-free closing process. When you’re weighing foreclosure vs selling for cash, having an experienced partner makes all the difference. We’re here to listen first and provide a clear, manageable solution that respects your privacy and your timeline. Request a confidential, no-obligation cash offer to stop your foreclosure today. You don’t have to face this alone, and a brighter financial chapter is within your reach.

Frequently Asked Questions

Can I sell my house if I have already received a foreclosure notice?

Yes, you remain the legal owner of your property even after receiving a notice of default or a notice of sale. You have the right to sell the home at any point until the hammer falls at the public auction. Taking a proactive approach in the foreclosure vs selling for cash debate allows you to present a concrete solution to your lender, which often pauses the legal clock while the sale is finalized.

Will selling for cash stop the foreclosure process immediately?

A cash sale stops the foreclosure process permanently once the transaction closes and the lender’s debt is satisfied. While simply signing a contract doesn’t legally freeze the process, most lenders will voluntarily postpone an auction if they receive a signed purchase agreement and proof of funds. This provides the bank with a certain path to repayment, which they usually prefer over the costs and risks of an auction.

Do I have to pay my mortgage during the cash sale process?

You are technically responsible for your mortgage payments until the day the property title transfers to the new buyer. However, since the goal of a foreclosure prevention sale is to resolve the debt, many homeowners let the sale proceeds cover the principal, interest, and late fees at closing. We coordinate with your lender to ensure the final payoff is handled correctly so you can move forward without further obligations.

What happens to my equity if the bank forecloses on my home?

In a foreclosure, your equity is often entirely consumed by the bank’s legal fees, default interest rates, and the low price typical of a public auction. Lenders only seek to recover the amount they are owed; they aren’t motivated to get you the highest price possible. Selling for cash before the auction date is the most effective way to preserve your equity and walk away with cash in your pocket.

Can a cash buyer help if I owe more than my house is worth?

Yes, we can help even if your home has no equity or is “underwater.” We specialize in creative finance solutions, such as taking over your existing mortgage payments through a Subject-To purchase. This method allows us to bring your loan current and handle the monthly payments, which protects your credit from a foreclosure mark without requiring you to pay anything out of pocket to sell.

How long does a cash sale take compared to a traditional sale?

A cash sale can be completed in as little as 7 to 14 days since it doesn’t require bank appraisals or mortgage approvals. A traditional sale on the MLS typically takes 60 days or longer and carries the risk of a buyer’s financing falling through at the last minute. When you’re facing a fast-approaching auction date, the speed and certainty of a cash offer are your strongest tools.

Is a cash offer always lower than a market listing price?

A cash offer is often lower than a retail listing price, but your net proceeds can be very similar. When you sell for cash, you don’t pay 6% in agent commissions, closing costs, or the thousands of dollars required for repairs and staging. You also avoid the mounting bank legal fees that grow every day you stay in the foreclosure process, making the “lower” offer a smarter financial move.

What are the tax consequences of selling for cash vs. foreclosure?

Foreclosure can trigger a “Cancellation of Debt” tax liability, where the IRS treats the forgiven portion of your loan as taxable income. A cash sale focuses on settling the debt through a private transaction, which can often mitigate these surprise tax bills. While you should always consult a tax professional, a voluntary sale generally provides a much cleaner financial exit than a bank-led repossession.